Quarterly risk assessment of the EU insurance industry

The Risk Dashboard, based on Solvency II data, summarises the main risks and vulnerabilities in the European Union’s insurance sector through a set of risk indicators.

The data is based on financial stability and prudential reporting collected from insurance groups and solo insurance undertakings.

Insurance Risk Dashboard April 2026 (Q4-2025 Solvency II Data)

Key observations:

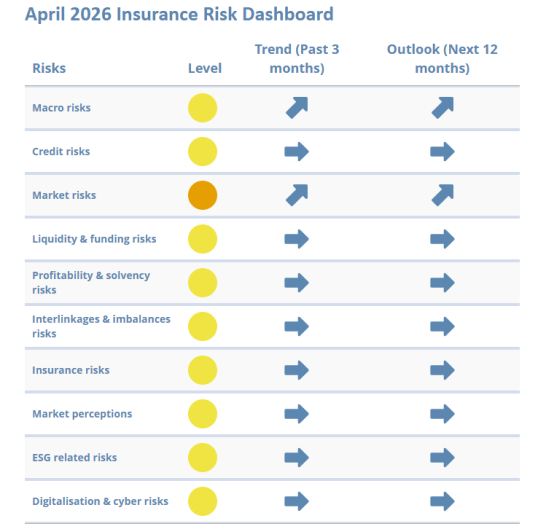

The April 2026 Insurance Risk Dashboard shows that risks in the European insurance sector are stable at a medium level.

- Somewhat higher inflation expectations, combined with persistent geopolitical tensions, continue to shape the macroeconomic environment. Uncertainty surrounding the conflict in Iran and its potential implications for energy prices may further amplify downside risks.

- Credit risks remain steady, with broadly unchanged fundamentals and high portfolio quality, despite some reallocation toward riskier bond segments and wider spreads.

- Increasing volatility in both bond and equity markets is driving a more elevated market risk outlook.

- Liquidity and funding conditions remain broadly unchanged, supported by stable cash and liquid asset and supportive lapse developments.

- Solvency and profitability risks are stable at a medium level, with modestly stronger capital positions and mixed profitability indicators.

- Strong premium growth and stable underwriting performance support a medium level of insurance risks, although uncertainty around marine, aviation and trade-related claims persists.

- Digitalisation and cyber exposures continue to shape the risk landscape. In the current geopolitical context, cyber threats remain a significant concern, adding complexity both to insurers’ operations and to the underwriting of cyber risks..

Go to the April 2026 Insurance Risk Dashboard

Note:

- The reference date for company data is Q4-2025 for quarterly indicators and 2024-YE for annual indicators. The cut-off date for most market indicators is the end of December 2025.

- The Level (color) corresponds to the level of risk as of the reference date, the Trend is displayed for the 3 months preceding the reference date and the Outlook is displayed for the 12 months after the reference date. The latter is based on the responses received from 23 national competent authorities (NCAs) and ranked according to the expected change in the materiality of each risk (substantial decrease, decrease, unchanged, increase and substantial increase).

Previous Dashboards

EIOPA's previous Insurance Risk Dashboards are available here.