Question ID: 3456

Regulation Reference: (EU) No 2015/35 - supplementing Dir 2009/138/EC - taking up & pursuit of the business of Insurance and Reinsurance (SII)

Topic: Own Funds (OF), Valuation of Assets and Liabilities other than TPs

Article: 15, 297

Status: Final

Date of submission: 06 Nov 2025

Question

The questions and proposed answers below are a follow up to question Q1 and Q2 (cat 1) of Q&A 2836, which were answered by the European Commission.

Sub-question 1

Question:

According to COM (answer to Q2), the ‘net deferred tax assets’ (net DTA) should be calculated as “the difference between the amount of deferred tax assets calculated in accordance with Article 15 and the amount of deferred tax liabilities against which the deferred tax assets may be set off.”

- From the answer of COM to question 1, we understand that “the amount of deferred tax assets (DTA) calculated in accordance with Article 15”, which is calculated by utilizing deferred tax liabilities (DTL) and/or (other future) taxable profits, requires a ‘detailed scheduling’ of the actual timing of these items.

- Regarding “the amount of deferred tax liabilities against which the deferred tax assets may be set off”, it is not explicit whether and in what way we should take into account the actual timing of the items that are involved (DTA and DTL).

Please note that DR Article 297, to which the above Q&A refers, does not contain any reporting requirements regarding deferred taxes anymore in the revised Delegated Regulation adopted by COM and published on 29 October 2025. At the same time, the revised Article 311(1)(e)(iv) DR on the reporting requirements regarding deferred taxes for regular supervisory report contains the following addition:

where net deferred tax assets shall be calculated as the difference between:

(1) the amount of deferred tax assets calculated in accordance with Article 15;

(2) the amount of deferred tax liabilities against which the deferred tax assets may be set off by taking into account detailed scheduling.

This seems to be the amendment following the assessment announced by COM in the answer to Q2. It is the same wording as in the answer by COM to Q2, except that in the 2nd item (the deferred tax liabilities) “by taking into account detailed scheduling” is added. Based on the explanatory memorandum and recitals, this is not a new requirement, but only a “streamlining” of the reporting requirements (p. 5 last bullet point ch 1, p.11 on SFCR and RSR, recital 41-45).

Q: can you clarify what is meant by “the amount of deferred tax liabilities against which the deferred tax assets may be set off”? For simplicity, we assume that all tax is levied by the same tax authority, there are no legal restrictions in offsetting due to the applicable tax law, and only timing needs to be considered (or not). We see the following three options:

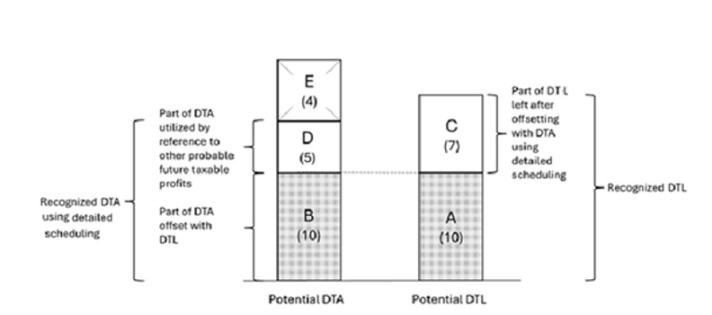

- The part of the DTL against which the deferred tax asset is offset when taking into account the actual timing of DTA and DTL. As a consequence, the net DTA then equals the part of the DTA, valued in accordance with Article 15, that is offset with other future taxable profits. In the figure that is introduced in the background information below, this means that the amount of DTL against which DTA may be set off is the amount denoted by letter A and net DTA equals B+D-A=D, which is equal to 5.

- The part of the DTL against which the deferred tax asset is offset when disregarding the actual timing of DTA and DTL, i.e. the whole of the recognized DTL. Net DTA then equals the DTA, valued in accordance with Article 15, subtracting the whole amount of the recognized DTL. In the figure that is introduced below, the net DTA equals B+D-A-C, which is (5 – 7 =) -2. Please note that in case the recognized DTL is larger than the recognized DTA (A+C > B+D), this will lead to a negative net DTA.

- The part of the DTL against which the deferred tax asset is offset (i) disregarding the actual timing of DTA and DTL like in option b, while (ii) preventing the possibility of a negative net DTA. Net DTA then equals the DTA valued in accordance with article 15 subtracted by the recognized DTL, floored at zero. In the figure that is introduced below, the net DTA equals max(B+D-A-C; 0) = max(D-C; 0), which is 0 in the example.

Sub-question 2

Question:

According to the EIOPA GL 9 paragraph 1.27, the recognized DTA and DTL can be offset (“netted”) under specific conditions. Regarding presentation on the Solvency II balance sheet, is there an obligation to offset DTA and DTL, given that it is required under certain conditions by IAS 12.74, but is not specified by Solvency II DR? And does this netting require “detailed scheduling”?

In other words, with reference to the figure above, should the DTA presented on the balance sheet only consist of part D and the DTL on the balance sheet only consist of part C, or can resp. B and A also be (partly) included?

Sub-question 3

Question:

It could be argued that the quantitative reporting template (QRT) “S.23.01 – Own Funds” contains the value of “an amount equal to the value of net deferred tax assets”, for which the ITS (S.23.01 – Own Funds, R0160/C0050) allow for further netting of the DTA and DTL presented on the balance sheet, in contrast to the reading of Article 15(3) DR presented above. What, if any, should be the relation between the values of DTA and DTL in the quantitative reporting template (QRT) “S.02.01 – Balance” and the values of “an amount equal to the value of net deferred tax assets” in QRT “S.23.01 – Own Funds”?

Background of the question

To further clarify this question, we’d like to make clear what we mean with the following concepts. The steps in which the concepts are defined, correspond to the steps that should be taken for the recognition and valuation of the DTL and DTA. For the sake of simplicity, we assume that current and past taxes do not play a role (“use of unused tax losses and unused tax credits”, Article15(3) Commission Delegated Regulation (EU) 2015/35).

- ‘Recognition’ of a DTA or DTL is meant in the sense of “ascribing a positive value” (Article 15(3) of Commission Delegated Regulation (EU) 2015/35) (for the DTA, but assumably the same applies to the DTL). The recognized DTA and DTL do not necessarily correspond to what is presented on the SII balance sheet (on the presentation, see question 4 and 5 below).

- The ‘basis of the DTA/DTL’ refers to (temporary) differences of the value of assets and liabilities for Solvency II purposes (“SII base”), i.e. on the SII balance sheet, and the value for tax purposes (“tax base”). These differences can potentially lead to the recognition and ascribing a value to a DTA or DTL. We hereby follow the wording of Article 15(2) of Commission Delegated Regulation (EU) 2015/35, that states that “Insurance and reinsurance undertakings shall value deferred taxes (…) on the basis of the difference between the values ascribed to assets and liabilities recognised and valued in accordance with Article 75 of Directive 2009/138/EC and in the case of technical provisions in accordance with Articles 76 to 85 of that Directive and the values ascribed to assets and liabilities as recognised and valued for tax purposes.”

- The ‘potential DTL’ refers to the valuation of the taxes potentially paid in the future over the basis of the DTL, in other words the tax that needs to be paid due to taxable temporary differences between the SII and tax base, as these differences lead to taxable profits in the future. The ‘potential DTA’ refers to the valuation of deductible taxes possibly recurred in the future over the basis of the DTA, in other words the tax that potentially can be recurred over the deductible temporary differences between the SII and tax base, as these differences lead to taxable losses in the future.

- ‘Future taxable profits’ refers both to future taxable profits included in the basis of the DTL, and future taxable profits that are not included there. We will use the term ‘other future taxable profits’ when referring to profits that are not included in the basis of the DTL (and are thus not taken into account in the valuation of the assets and liabilities on the SII balance sheet). This follows from Article 15(3) of the Commission Delegated Regulation (EU) 2015/35, which requires that “Insurance and reinsurance undertaking shall only ascribe a positive value to deferred tax assets where it is probable that future taxable profit will be available against which the deferred tax asset can be utilized”, where the DTA can both be utilised by means of available DTL as well as by other future taxable profits, taking into account any legal or regulatory requirements.

- ‘Projection of future taxable profits’ as used in Guideline 9, 1.29 of the Guidelines on recognition and valuation of assets and liabilities other than technical provisions (EIOPA-BoS-15/113), refers to projections performed to derive ‘other future taxable profits’, i.e. future profits outside the SII balance sheet.

Based on these concepts, and in order to further specify our question regarding the calculation of the net DTA, the following steps are taken in the recognition and valuation of the DTA and DTL. These steps are also in line with Guideline 9 paragraph 1.28 of the EIOPA Guidelines on recognition and valuation of assets and liabilities other than technical provisions.

As a first step, the potential DTL and DTA are determined. For this, the temporary valuation differences are identified, which form the basis of the DTL and DTA. Next, the potential DTL / DTA is calculated by subtracting from the basis of the DTA/DTL the (temporary) differences that do not lead to taxable profits / losses (e.g. because they are exempt from tax), and by multiplying the result, i.e. the taxable / deductible temporary differences with the applicable tax rate. Please note that for simplicity we assume to have one applicable tax rate only. The potential DTL is immediately recognized as DTL, since the articles in the Commission Delegated Regulation (EU) 2015/35 do not contain further conditions on which this recognition depends. However, for the recognition of the potential DTA as DTA, a substantiation is required that demonstrates that the deductible losses of the potential DTA can actually be recurred. This is done in the subsequent steps.

As a second step, the timing of the reversal of the taxable / deductible temporary valuation differences is determined. In this step, the taxable profits and taxable losses resulting from the reversal of the temporary valuation differences that form the potential DTL and the potential DTA can be offset (or netted) if they occur in the same period, or if the deductible loss leading to the potential DTA can be carried back or forward taking into account any legal or regulatory restrictions. This is in line with the concept of ‘detailed scheduling’, as described in Article 15(3) of Commission Delegated Regulation (EU) 2015/35 and IAS 12 paragraph 28, to which the answer from the European Commission to question Q1 refers.

Thirdly, the value and timing of the probable future taxable profits are determined, especially of the other profits that are not included in the basis of the recognized DTL, provided they relate to the same taxation authority and the same taxable entity (IAS 12). According to Article 15(3) of Commission Delegated Regulation (EU) 2015/35, the DTA can only be recognized “where it is probable that future taxable profits will be available against which the deferred tax asset can be utilized”. As “future taxable profits” refers both to profits included in the recognized DTL and profits that are not (see above), the recognized DTA consists of a part that is offset with the DTL (as was done in step 2 above) and a part that is offset with other future taxable profits. Just as for offsetting with the DTL, offsetting with other future taxable profits is only possible if they occur in the same period as the reversal of deductible temporary valuation differences that form the potential DTA, or if the deductible loss leading to the potential DTA can be carried back or forward taking into account any legal or regulatory restrictions, again in line with the concept of ‘detailed scheduling’ in Article 15(3) of Commission Delegated Regulation (EU) 2015/35 and IAS 12 paragraph 28. It is possible that a part of the potential DTA cannot be offset with any future taxable profit, and therefore cannot be recognized.

The steps mentioned above can be summarized in the following figure. The bars show the potential DTA and DTL. The recognized DTL equals the potential DTL. The parts of the DTL and the DTA that can be offset are indicated as components (A) and (B) in the figure respectively. The remaining part of the recognized DTL is indicated as component (C). (For the question what part of the DTL should be presented on the balance sheet (A, C or something else), see question 4 below.) The part of the potential DTA that is offset with other future taxable profits is component (D). The part of the potential DTA that cannot be offset with future taxable profits and cannot be recognised is component (E) in the figure.

Let’s assume that component A and B are both equal to 10, component C is 7, component D is 5 and component E is 4. This means that the potential DTA is (10 + 5 + 4 =) 19, the recognized DTA is (10 + 5 =) 15, and the potential DLT equals the recognized DTL and equals (10 + 7 = ) 17.

EIOPA answer

Sub-question 1:

The meaning of “the amount of DTL against which the DTA may be set off” is the amount of DTL that can be used to recognise DTA while taking into account, inter alia, detailed scheduling, in accordance with Articles 9 and 15 of Commission Delegated Regulation (EU) 2015/35 and further specified in Guideline 9 of EIOPA’s Guidelines on the recognition and valuation of assets and liabilities other than technical provisions. As clarified by Q&A 2836, a necessary but not sufficient condition to recognise a DTA is the assessment of the detailed scheduling of the DTA with respect to DTL and/or other future taxable profits that can be used to recognise such DTA. In line with the calculation of the DTA, this requirement of detailed scheduling extends to the calculation of the net DTA, see also Article 311 (1) (e) (iv) of Commission Delegated Regulation (EU) 2015/35 revised under the Solvency II Review.

In the example of the question, the following quantities A, B, C, D, E are defined. Furthermore, the example assumes for simplicity that all other requirements are satisfied, and only the condition of detailed scheduling of the timing of the reversal of DTL and/or of the timing of other future taxable profits needs to be considered, i.e. in the example this condition is necessary and sufficient.

- B+D+E = 19 is the calculated amount of DTA without an assessment of their probable utilisation, i.e. without assessment if a positive value can be ascribed. For simplicity, this will be referred to as “potential DTA” in this Q&A.

- A+C = 17 is the calculated amount of DTL, which coincides with the recognized amount of DTL, in line with Article 15 of Commission Delegated Regulation (EU) 2015/35.

- E = 4 is the part of the potential DTA that is not recognised, as failing to comply with the requirement of Article 15(3) of Commission Delegated Regulation (EU) 2015/35.

- B = 10 is the part of the potential DTA that is recognised, as it complies with Article 15(3), and that is fully offset by the DTL A = 10, taking into account the timing of the reversal of DTL.

- D = 5 is the part of the potential DTA that is recognised as it complies with Article 15(3) and whose recognition is supported exclusively by other future taxable profits and not by the reversal of any DTL.

- C = 7 is the part of the DTL that cannot be used to offset any DTA.

Hence, the recognised DTA, taking into account inter alia the detailed scheduling of DTLs and/or other future taxable profits, are equal to B+D = 15.

Under these assumptions, in line with Q&A 2836, the net DTA are equal to D = 5. Furthermore, this conclusion is consistent with Article 311(1)(e)(iv) of the amended Delegated Regulation that will be applicable from 30 January 2027. Options b and c in the question are not consistent with Q&A 2836 and the relevant legal articles, as they erroneously offset DTA and DTL disregarding the detailed scheduling.

Finally, the net DTA may contribute to the Tier 3 Own Funds subject to the provisions set out in Article 76 and 77 of the Commission Delegated Regulation (EU) 2015/35. In particular, the item “an amount equal to the value of net deferred tax assets” mentioned in Article 76(a)(iii) shall be classified as Tier 3 where it possesses all of the features set out in Article 77(1)(b) and (h). Consequently, the net DTA that is recognised as Tier 3 Own Fund item in the example might be further reduced (e.g. becomes smaller than 5), if the full amount does not fulfil the criteria to be classified as Tier 3 Own Fund item (see also sub-question 3).

Sub-question 2:

In our understanding, the question refers to the reporting of DTA and DTL in the quantitative reporting template (QRT) S.02.01, hence this answer pertains solely to the presentation of these items. Our answer does not concern or introduce any requirements to the recognition and valuation of deferred taxes, which should be carried out according to accounting practices subject to the provisions set out in Articles 9 and 15 of Commission Delegated Regulation (EU) 2015/35 and further clarified by Q&A 2836 and in the response to the first sub-question of this Q&A.

In line with the definition of DTA and DTL in Commission Implementing Regulation (EU) 2023/894 and the general principles of valuing assets and liabilities separately set out in Article 75 of Directive 2009/138/EC and Article 9(5) and (6) of Commission Delegated Regulation (EU) 2015/35, DTA and DTL calculated according to Article 9 and 15 of that Delegated Regulation should be reported separately in QRT S.02.01, i.e. , without offsetting between the two. To this purpose, please note that Commission Implementing Regulation (EU) 2023/894 defines DTA and DTL (R0040 and R0780 in QRT s.02.01) in a way that is identical to the general definition of DTA and DTL in IAS 12, before IAS 12 considers any offsetting between the two for presentation purposes (i.e. the presentation of DTA and DTL follows the valuation). Under the assumptions of the example addressed in the first sub-question, the DTA in row “R0040” is equal to B+D = 15 and the DTL in row “R0780” is equal to A+C = 17.

Furthermore, this is consistent with the clarification provided in Q&A 2836. While IAS 12 for presentation purposes requires to offset DTA and DTL subject to some conditions and in some cases without detailed scheduling (e.g. in IAS 12.74 and 12.75), the response to the first question of Q&A 2836 clarifies that IAS rules related to the presentation (and not the valuation) of results are not relevant for Solvency II (i.e. the presentation of DTA and DTL should be performed following the valuation, and it should not influence the approach taken in accordance with the Solvency II valuation requirements).

Sub-question 3:

As explained in the answer to sub-question 1, Q&A 2836 clarifies that for the calculation of the net DTA detailed scheduling should be taken into account. Moreover, the European Commission has adopted amendments to Commission Delegated Regulation (EU) 2015/35, which, in Article 311, further clarifies this requirement regarding net DTA. As a consequence, as also demonstrated in the example of sub-question 1, the reported net DTA (D = 5) do not necessarily correspond to the mathematical difference between the recognized DTA and DTL (B + D – A – C = 15 - 17 = -2).

Moreover, the net DTA can only be classified as Tier 3 own funds and hence reported in QRT S.23.01 as far as they comply with the provisions set out in Article 76 and 77 of Commission Delegated Regulation (EU) 2015/35. In particular, the item “an amount equal to the value of net deferred tax assets” mentioned in Article 76(a)(iii) shall be classified as Tier 3 where it possesses all the features set out in Article 77(1)(b) and (h).

Consequently, the net DTA reported in QRT S.23.01 may be further reduced with respect to the calculation in the first paragraph. By reference to the example, this means that the reported net DTA is equal to or smaller than 5. In the case, different from the example, that all DTL can be used to offset the DTA, this means that there can be instances where the net DTA reported in QRT S.23.01 are smaller than the simple mathematical difference between the amounts of DTA and DTL.